I'm still here, no suicide livestream, I've just been breathing/decompressing for a bit as this XIV/SVXY show hit me a little harder than I planned for a few reasons, mostly conceptual-

The #1 takeaway I'll put first- from the UVXY/VXX and /VX action after 2/5, it looks like the life thesis of the short vol trade endures. Lets give it a month or 6 and see where we are at.

Now the XIV/SVXY issue-

This hit me hardest as I came in the last 2 years with the plan of having small defined risk positions and waiting for these good pot odds situations to scale in. I don't know how many excel sheets of weekly, monthly yearly price and % moves I've looked at in every product, and of course pretty much every article and interview on them.

One of the 'conservative' Vol strats I've seen backtested a lot on quantopian, etc is XIV buy and hold with a certain portfolio % after such 16, 20 , or higher VIX spikes which we finally got.

In my own backtesting and referencing across all these other resources, XIV/SVXY went perfectly through 2011, 2015 flash crashes, S&P 10% downmoves and VIX popping to 50, getting about a 50% decline in the most extreme of these market moves,

which I showed in one of my earlier articles.

The main pain of this whole thing is that VXX and UVXY seem to be working perfectly in comparison. Due to the option spreads during big VIX spikes in these products it makes more sense to just get stock. The final dagger is the majority of the 'move' happening in 15min of aftermarket trading.

I have to admit

I made a big mistake, I got a tranche of stock (covered call) too many in SVXY on the 5th trying to catch the falling knife..

Like I've written before its just like poker or chess where 99% of the game plays in a certain 'range' such as raise fold, 3 bet fold, C bet fold, and then in a 5 hour session your entire P/L comes down to one huge hand of nuts vs 2nd nuts on the river. A GM chess game is 6 hours of perfect moves back and forth, dead even until one move misses a 7 move tactic and the game ends immediately, there is no ebb and flow back from there. Even though it was a huge risk management mistake, I still felt double headshot because I had to be in SVXY with that mistake to get the full decapitation. Here is my 2/5 flowchart-

I think it was more impatience than greed, but I then mused that

impatience is just greed for time, and time and money have their own dynamic exchange rate, so impatience really is greed. What a failure..

"Fortunately" this was SVXY and not XIV, but it seems like fate anyway, as I'm only in it for the option chain, what if XIV with the 80% termination clause had options and SVXY with the discretionary clause didn't?

If I just took the exact same directional risk/position sizing in UVXY/VXX on the Feb 5th dip the P/L this year would be 2 different planets (see above flowchart). Some of my short vol positions were VXX, UVXY spreads going into the 5th, and given the duration and potential rolling out these might be salvageable, but the equivalent SVXY short put spreads at the time definitely are not and did not behave like any backtesting in the history of the product.

VXX/UVXY takeaways? - Should we be spreading position risk across multiple similar products just to hedge such a failure? In a way I did have this but between UVXY, VXX and SVXY I was heaviest in SVXY due to waiting on the UVXY reverse split. (One of my ironically most prophetic moments)

All the ideas of long SVXY/XIV having the least amount of duration risk vs 60day+ VXX, UVXY spreads, all means nothing.

One final point on the "

manipulation" articles that came out: I think that could definitely be possible, with a 10 year product disappearing in 15 minutes during the tiny futures window overlap. Even if you agree there is no 100% evidence out yet, I think refusing to believe that its possible is just too 'head in the sand' given the libor and metals manipulations over the last 5-10 years. The main point is that the manipulation shouldn't matter, it was my risk management that killed me right at the end. A good strategy and psychology should endure through something like that with enough duration/delta/product diversity/cash to take a bump like that.

One of the 2nd main takeaways from this is that I'm trying to not throw it all away and turn too cynical like the Zerohedge comments section who drool for years to get a story like this. I still believe in short VIX and all the market action in a week since the 5th agrees with me.

Short VIX takeaways for this year and beyond:

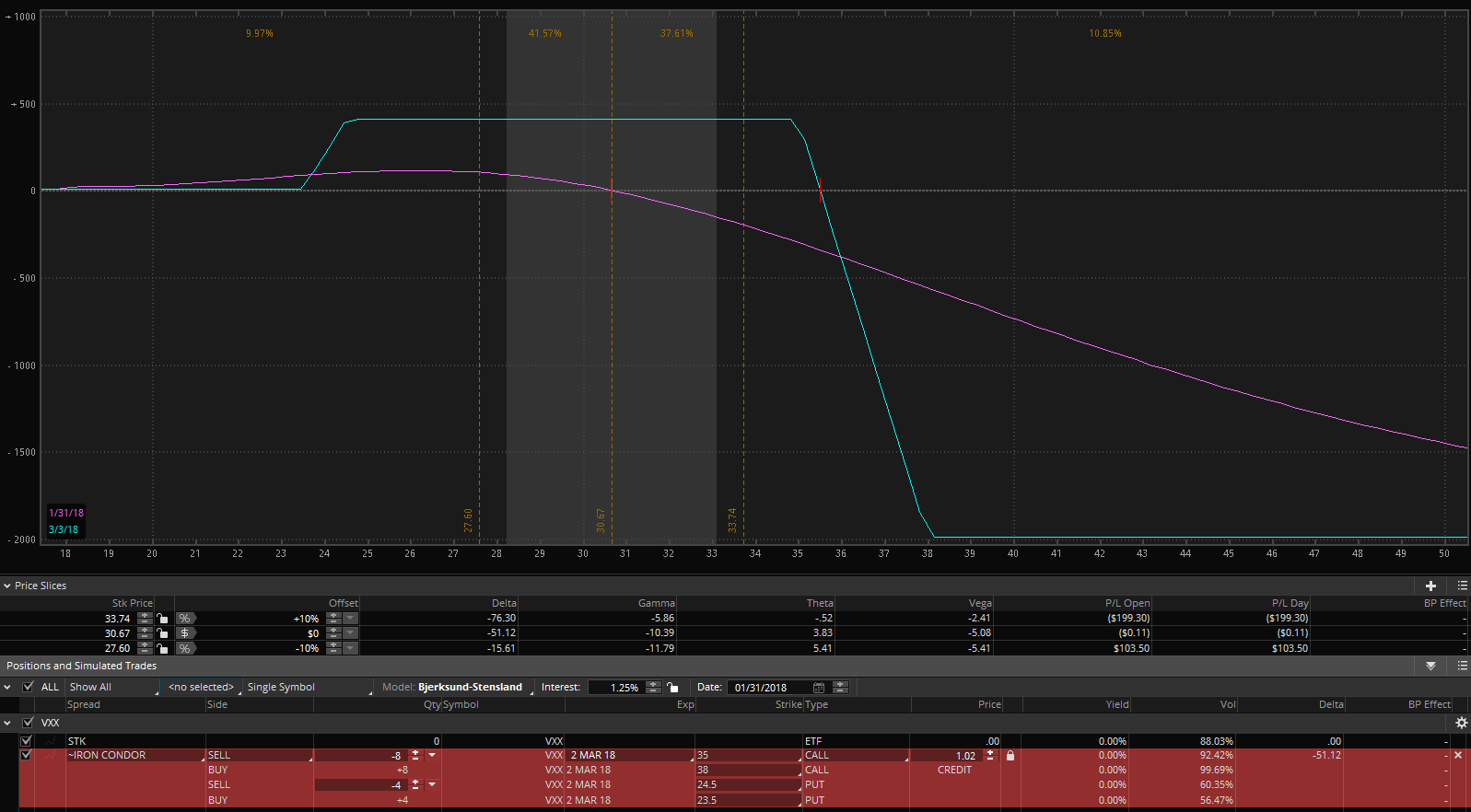

This year looks fully wrecked, so I'll just be chipping away with short vol positions, slightly slanted more on the "soft cap iron condor" side adding a little risk to the vol short side because of how much contraction I could use now. In the few days after 2/5, I got some VXX short put spreads a little over 30% OTM for the month, which backtested for all of VXX only happened once or twice hitting 32% decay (which I should be at with the net premium). Its dark even mentioning this because we just saw the folly of trading based on the entire backtested history of a product, but if we give up on any data we have then what is the point of any of it/

Beyond the recovery trajectory, if you just think about short VIX in a vacuum if you are starting now, its an incredible pot odds time to short VIX, and more importantly a huge blow up like this gives the bears and long VIX crowd a dream to cling to for another 5-10 years. I know

I messed up this year, but this makes the next 5 years that much better- for me and everyone. Again I'm trying to think of a long term investment strategy- asset class wise

and in terms of improving myself.

(Yes of course SPY can and probably still will crash more this year but that doesn't change the pot odds of shorting VIX with spot way over the 'long term average' and above the whole year of futures pricing)

Sorrow takeaways:

For the last week I've had so much chest pain I couldn't shake, even though I know the trajectory of Vol going forward should go down. I know it could've been worse, I could have made a bigger mistake, and intellectually I know I'll be fine and life goes on, just my heart doesn't know yet. I need to get through this chest pain and get it all back to normal.

A little of this whole rambling is just to my one reader.. don't give up on me yet. I just want to get back to my routine of twitter and all the market news sites and getting back to MSpainting Jay Powell, there is so much work to do.

This was like another Janet break up where we just need to get back on track, let the scars heal, and in time it will just be a blip on a huge chart.

One more sorrow bit, with the last week or two of crypto action which I could take no pleasure in. Watching Bitconnect and others fully blow up as expected was bittersweet as XIV blew up, because to outsiders

these are just the same thing. If you tell someone XIV or BCC lost 99% they just say 'oh so thats like a scam/penny stock/ponzi/whatever'? There's no retort really, we just have to breath and know the market vol mechanics.

I feel like I've let short VIX down, like I don't deserve the name right now because I just made a stupid trade, it might as well have been going all leveraged on long options around some AMD earnings or going all in on some crypto before an announcement. I just made an emotional mistake almost unrelated to VIX. This was an XIV/SVXY problem but it was more a

me problem.

Half of this feels like some stupid youtube apology video, and I think the whole situation will only get better with time. Making mistakes is part of the short VIX life metaphor, just don't make one all-game over mistake, and ride out the smaller mistakes/jumps/spikes/fear. Its an important growth experience, and I hope you will accept me back in your heart-